Working capital ratio for inventories availability

The working capital ratio for inventories availability (WCRIA) and expenses shows a share of inventories and expenses financed from own sources. This is one of the indicators for determining the financial stability of the company and an indicator of the state of working capital. It is the ratio of the equity to the value of inventories and costs which cover by equity.

Economic meaning of indicator and formula

The working capital ratio for inventories availability and expenses reflects a portion of the inventories and costs that are purchased from equity. To find the indicator you should divide the value of own funds by the valuation of inventories and costs.

The conventional formula looks like this:

WCRIA= net working capital/inventories

The indicator in the numerator is called "working capital". This value reflects how much current assets are greater than the company's short-term liabilities. Net working capital shows the company's ability to repay short-term obligations after the sale of its current assets. That is, "working capital" is an indicator of the company's solvency and financial stability.

Net working capital is the difference between mobile assets and short-term accounts payable. If you detail the components of "working capital", then the calculation of the ratio of working capital will look different.

The formula:

WCRIA = (WA – STL) / inventories and expenses

- WA – working assets;

- КО - short-term liabilities.

You can calculate the value in the numerator using another way. Then the formula for the working capital ratio for inventories availability and expenses will look like this:

WCRIA = ((E + LTL) – NCA)) / inventories and expenses

- E – equity;

- LTL – long-term liabilities;

- NCA – non-current assets.

Different variations of the calculation formula are used in financial practice. In particular, the composition of working capital includes unpaid dividend, unearned revenues, reserves for future expenses and payments. The size of inventories can be supplemented by advances to suppliers, work in process.

Calculation of working capital ratio of inventories availability in Excel

Data for calculating the ratio are taken from the balance sheet. We transform the formula:

WCRIA = (1300 + 1400 – 1100) / 1210

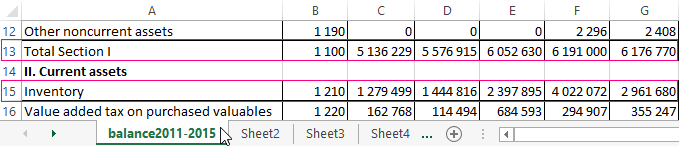

We need next figures from different balance sheet line codes:

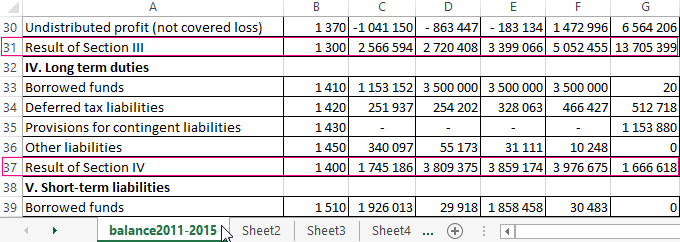

And we need such line codes from liabilities as:

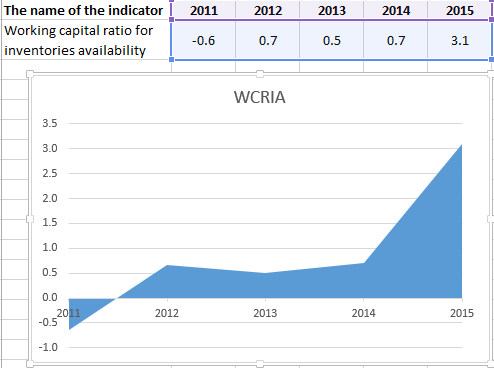

We calculate the indicator for 5 reporting periods, from 2011 to 2015:

The negative value of the coefficient in 2011 is explained by the negative value of its working capital. Normally, it should be above zero. That is, current assets should exceed short-term liabilities.

A negative value of working capital indicates financial instability of the company. But such a criterion cannot be applied to all industries. There are enterprises that successfully function even with a negative indicator. For example, a notorious McDonalds company from the fast food industry. Ultra-fast operating cycle almost immediately transforms inventories into cash proceeds. That’s why a negative value of own circulating assets is not felt.

The working capital ratio for expenses availability is the result of a comparison of the last one with the size of the inventories. The optimal condition and indicator of financial well-being is the excess of working capital over inventories.

The matter is that inventories are the least liquid part of working capital. Therefore, they must be repaid by equity and/or using the long-term liabilities.

Working capital ratio for inventories availability and criterion value

The norm of the indicator is in the range between 0.6-0.8. That is, 60-80% of the material reserves should be financed through equity. The higher the indicator, the less the organization needs in liabilities. In a word, if the working capital ratio of inventories availability is higher than the norm, the financial stability of the company is higher; and if lower than the norm, it becomes necessary to use liabilities.

Let's return to the example. Dynamics of the coefficient on the chart:

The calculation shows that from 2012 the inventories and expenses are sufficiently provided by own sources of capital. The growth of the coefficient positively affects the financial stability of the firm.

Data Visualization Charts for Interactive Report Creation in Excel.

Dashboard Templates